Speak with a Reverse Mortgage Expert

Reverse Mortgages to Fit Your Lifestyle

A large percentage of Americans are under saved for retirement and with the rising cost of housing, increasing cost of health care, and overall uncertainty, navigating retirement decisions has become uniquely challenging and often overwhelming. Although home equity typically represents over 70% of net worth, it is most often disregarded as a retirement asset. Accessing this equity through a Reverse Mortgage could be one of the most misunderstood and underutilized strategies in retirement planning today.

Through a Reverse Mortgage, homeowners may be able to extend the longevity of their cash flow, ensuring they don’t run out of money. Through a Reverse Mortgage line of credit, homeowners can increase their access to liquidity and reduce withdrawals from investment accounts to continue building their asset portfolio. With a well-designed plan that includes accessing home equity, financial professionals have been able to increase legacy assets left for children, family members, or other important causes.

Your home. Your lifestyle. Your retirement. A Reverse Mortgage may be the answer to provide you with both certainty and flexibility, to live life on your terms.

Reverse Mortgages Calculator

Estimate the home equity you may be able to access with a Reverse Mortgage

This calculator is meant to be for demonstration purposes only.

Types of Reverse Mortgages

Home Equity Conversion Mortgage (HECM)

Designed by HUD and insured by the Federal Housing Administration (FHA), the home equity conversion mortgage (HECM) is the most common Reverse Mortgage in the marketplace.

Features of the HECM:

- Access to equity available through a revolving line of credit in which the available credit increases monthly

- FHA insured to protect access to equity, tenure payments, as well as borrower’s estate and heirs from any deficiency when loan is settled

- No minimum credit score requirements

- Available to individuals or spouses as long as one meets the minimum age requirement of 62

- Loan must be secured by a primary residence and in first lien position

- Loan becomes due and payable when the home is sold, last borrower passes away or moves out of the home for 12 consecutive months, and/or homeowners fail to meet the terms of the loan obligations

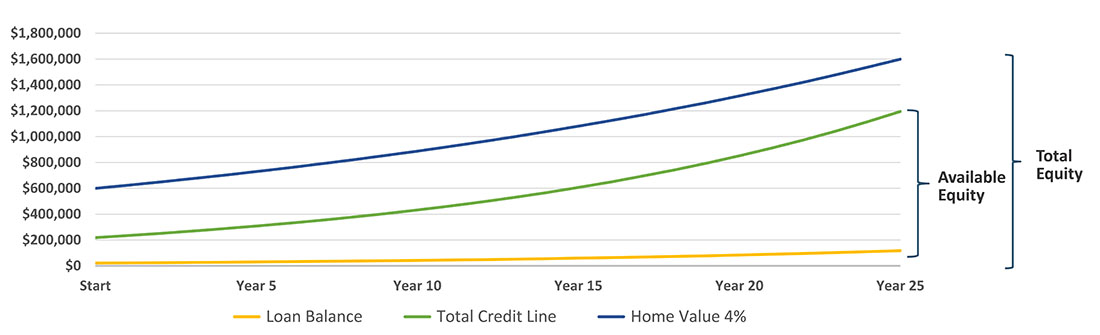

Line of Credit Growth

55+ Specialty Reverse Mortgage

For homeowners with higher valued homes, typically beginning at or above $1 million, a 55+ specialty Reverse Mortgage may be a consideration. With higher lending limits and lower age requirements, these programs may provide additional options.

- Loan amounts up to $4 million

- Minimum age requirement of 55 or above in select states

- Available in single lump sum distribution or line of credit

- No mortgage insurance requirement

Reverse Purchase Mortgage

For families looking to move or purchase a home, a reverse purchase could provide additional flexibility and purchasing power to enhance retirement opportunities. Available through the HECM program as well as the 55+ Specialty Mortgages, borrows have more options than ever before.

A few reasons to consider a reverse purchase:

- Finance your home purchase without the burden of a monthly mortgage payment

- Increase purchasing power over an all-cash purchase while still avoiding payment obligations

- Afford more home with the same cash investment

- Maintain investment balances with flexible financing rather than taking withdrawals for cash purchase

- Improve retirement cash flow over a traditional mortgage

Common Uses of a Reverse Mortgage

There are many uses for a Reverse Mortgage to improve retirement outcomes.

Eliminate Mortgage Payments

Purchase a Home with a Reverse Mortgage

Home Improvements and Modifications

In Home Care Expenses

Bridging Social Security Benefits

Increase Cash Flow

Tax Strategies

Many Others!

How Do Reverse Mortgages Work?

A Reverse Mortgage is similar to a traditional mortgage with a few very important exceptions.

Optional Mortgage Payments

Unlike a traditional mortgage that requires monthly payments, with a Reverse Mortgage, payments are optional. Borrowers can make payments as often or in any amount that they choose. They can also elect to never make a payment. Like a traditional loan, homeowners are still required to remain current on property taxes, homeowner’s insurance, homeowners’ association fees and to maintain the property.

Receive Payments from your Loan

For homeowners with sufficient equity, they can elect to receive monthly payments from the loan. This can be paid as a set amount for life, over a specific term, or as periodic withdrawals. Because the payments are loan proceeds, they are not counted as taxable income.

Not a Specific Term of Years

Whereas traditional loans have a set number of years for repayment, a reverse loan is based on the borrowers living in the home. The loan doesn’t need to be repaid until the last borrower moves out of the home permanently, the home is sold, or homeowners fail to meet the terms of the loan obligations.

Occupancy

Unlike traditional loans where the property can be either owner occupied, rental, or second home, a Reverse Mortgage requires the home to be owner occupied for the full term of the loan.

Non-Recourse Loan

If the borrower chooses to not make payments and in the event the loan balance increases beyond the value of the home, neither the borrower, their estate, nor their heirs will not be responsible for the loan balance beyond the home value.

Limited Income Requirements

Since borrowers are not required to make mortgage payments, there is a lower income requirement to qualify for a reverse loan. Known as “residual income,” a financial assessment is taken to ensure borrowers can meet the obligations of their property taxes, homeowner’s insurance, and basic needs to maintain the home. This is commonly a much lower income amount than is needed to meet traditional mortgage requirements.

Third Party HUD Counseling

To make sure borrowers have been accurately informed about the terms and conditions of a Reverse Mortgage, they are required to speak with a certified HUD counselor prior to proceeding with the loan process. This adds a layer of protection so no important information is overlooked.

Benefits of a Reverse Mortgage

Reverse Mortgages are insured by the Federal Housing Agency (FHA) and can provide additional financial security while allowing senior homeowners to stay in their home.

- No monthly mortgage payments required

- Continue to live in and own the home

- Home must be the principal residence

- No income limitations

- Non-recourse loan protection

- Your home must meet minimum property standards set forth by HUD

- Required independent, government-approved housing counseling

- They are only available to homeowners who are 62+

- No minimum credit score requirements

Buy your Dream Home with a Reverse Mortgage

1.

Contact a reverse mortgage specialist to discuss your qualifications and the amount needed for a down payment.

2.

Begin your home search and start the reverse mortgage application process, which your loan officer will help walk you through.

3.

Once you complete the loan process, you’ll be the owner of your new home with the option for no monthly payments.

Refinancing your Reverse Mortgage

1.

Talk to a Reverse Mortgage professional to your loan officer to determine if refinancing will offer you financial benefits in the long-term.

2.

Your loan officer will confirm if you meet the loan requirements depending on the type of reverse mortgage you’re applying for and assist you through the loan application process, which includes obtaining an appraisal for your home and submitting necessary financial documentation.

3.

Once your loan is approved, you’ll close by reviewing your final loan documents, and selecting how you will receive your funds moving forward.

Common Reverse Mortgage Questions

Will the bank take title of my home?

No. A Reverse Mortgage lien is treated the same as a traditional loan. The lender will take a lien on your home but you will maintain ownership.

Will a Reverse Mortgage affect my Social Security benefits or pension benefits?

No, these benefits are not affected by a Reverse Mortgage. In fact, many financial advisors work with their clients to use a reverse line of credit to delay drawing social security benefits, which could boost your lifetime retirement income.

How much money can I get?

The amount you can receive is based on a few variables like the age of the youngest borrower, the appraised home value, interest rates, and, in some cases, FHA lending limits.

How does interest work with a Reverse Mortgage?

Borrowers are only charged interest on funds they have received, known as your outstanding balance. If borrowers choose not to make payments, the interest will accrue on the loan.

Aren’t Reverse Mortgages for people that have exhausted all other resources?

No! More than ever, financial professionals are recommending Reverse Mortgages be taken earlier in retirement, long before there’s a “need.” This creates options and flexibility for improving long term cash flow, reducing income taxes, providing access to liquid assets, and in many cases, increasing inheritance amounts to heirs.

What if I already have a Reverse Mortgage?

If you already have a reverses mortgage, you could be eligible to refinance your loan. With higher home values and increased lending limits, many homeowners are able to access additional equity. In many cases, upfront fees are reduced based on what you paid when you originally completed your loan.

How can I learn more?

Every situation is different. To learn more about how a Reverse Mortgage could improve your retirement outcomes, please connect with our team of Reverse Mortgage professionals and Equity Wealth Strategies team. With extensive experience in evaluating retirement strategies, they will invest time to understand your overall situation, can work together with your family or other advisors, and help determine if a Reverse Mortgage is a good fit for your family.